Putting the engine in the driver’s seat – a look into the future insurance business setup

• The traditional strategy process in antiquated as technology is changing the world at extreme pace and renders core competences worthless overnight

• A deep understanding of the technological development and impact should be forming the basis of the insurers’ strategies

• Tech development, impact and implications must be part of the permanent Board agenda

• The new role of the head of technology explained

• How will the future insurance delivery model look like?

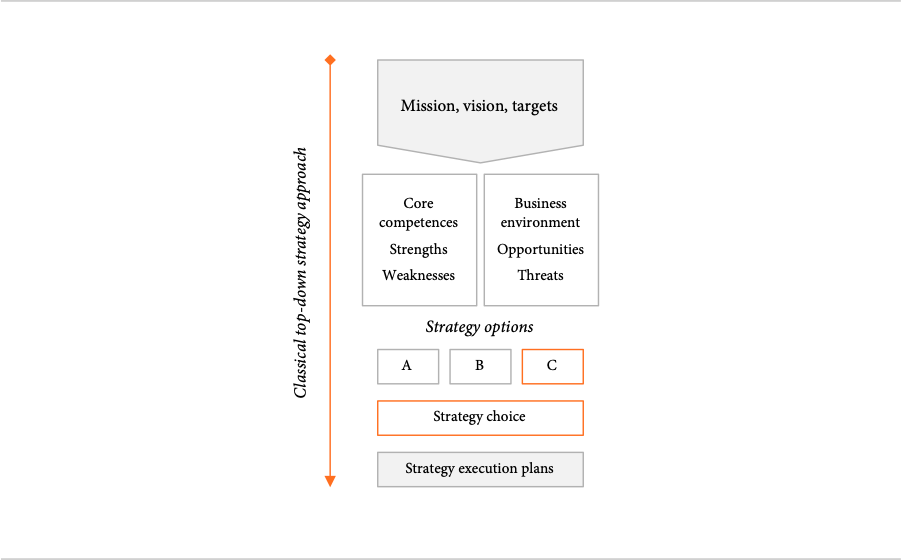

Traditionally, strategy development has been a top-down process, starting with the mission and vison of the company and a financial target, adding internal and external analysis to determine the firm’s capabilities and the characteristics of the business environment – most often resulting in the SWOT analysis, identifying the company’s strengths and weaknesses and the opportunities and threats in the market

In most cases, articulating the firm’s core competences as defined by Prahalad and Hamel is a part of the strategy exercise as these traditionally play an important role in defining the company’s competitive advantage in the market

Figure 1: The traditional top-down strategy process

Following the analysis, a series of strategic options have been defined and the most attractive in terms of cost/benefit and chance of success selected, followed by the creation of high-level plans, in turn cascaded to the business units to develop detailed execution plans

This strategy process is a solid and well-proven tool for companies operating in stable and fairly predictable environments but comes under stress in fast-changing and unpredictable operating environments. It’s safe to state that the insurance industry has been a very stable and predictable environment, where even the rise of the insurtechs has not been able to disturb the industry significantly

However, there are several signs that this is about to change as new entrants, distribution models, products and services offerings are slowly entering the insurance industry – all of them now with an accelerated pace caused by the global pandemic, forcing customers to stay home and turn to virtual and digital solutions

This not only changes the speed of market development and unpredictability; it also threatens to render some insurers’ core competences useless – think of an insurer with a large and well-positioned branch network as core competence. The lockdown of many countries and stay home directives have forced all customers to use digital tools for their insurance needs. From home

Overnight, the branches as core competence has been transferred into a heavy cost burden for the insurer and no longer a key competitive factor in the market

Products and distribution channels are being challenged by insurtechs leveraging insurers’ and reinsurers’ capacity to offer digital ways of buying insurance, often with attractive changes to the premium calculation (usage-based-insurance, pay-as-you-go, etc.). While this may not seem threatening at the moment let alone disruptive, customers are seeing what is possible, which increases their expectations to even basic insurance products, services and premium calculation models

A new baseline for minimum requirements for insurance products is slowly being set and the pandemic-accelerated worldwide focus on digital product and systems acceleration will only increase the speed of change in customer expectations

Crafting the insurer’s three-year strategy plan based on a model that has proven its worth in known markets with predictable development for decades no longer seems like a viable option for creating a future direction for the insurance company

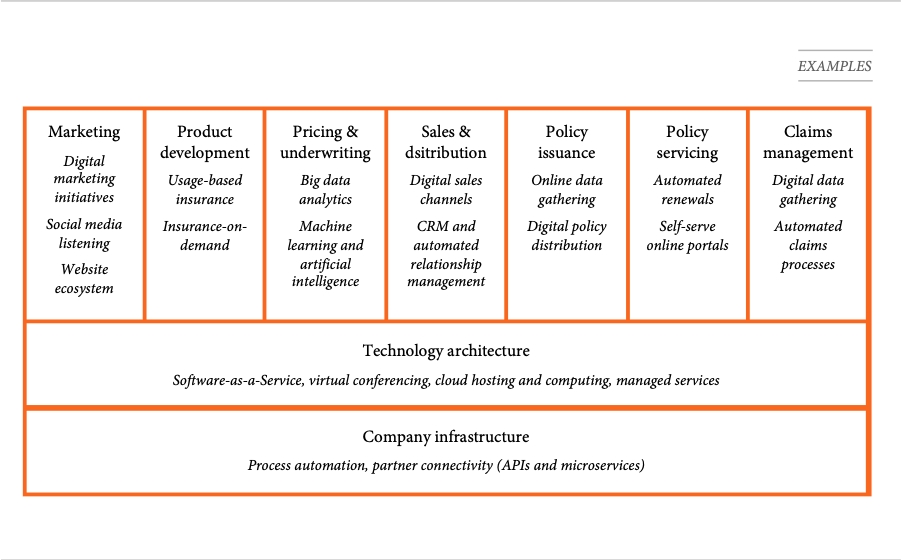

Tech is in everything

Discussions on IT in insurance has a tendency to revolve around legacy IT systems, old applications and a very rigid structure, that takes years to adapt and adjust to market changes. This may to some extent be the situation of many insurers today, but even held back by legacy systems, technology is still permeating the insurance value chain

Figure 2: There is already technology in all elements of the insurer’s value chain

It is difficult to imagine any new products, services or processes being created without an element of IT and technology, and it seems safe to say that technology is now driving business success. If the technology is not a central part of the business, there will be competitors utilizing technology to offer better and more flexible solutions, faster and most likely cheaper

However, many of the tech initiatives and services are not interconnected and acts as satellite IT systems and applications – this is one of the major reasons insurers feel the lack of speed and inability to change digital pace fast, and a key focus area to be resolved going forward

More on this later in this whitepaper

As discussed in the whitepaper Insurtechs, a part of insurers’ digital transformation?, there are many digitally advanced products and services that insurers can leverage to get a competitive advantage but integrating these into the overall digital portfolio of the insurer requires significant changes and organizational adjustments. All driven by IT development

Figure 3: The software and application lifespans are constantly decreasing

Fueling the requirements of adapting increasingly faster to a digital world is the speed of technological development; the software S-curve is getting increasingly steeper as software and applications moves through the entire lifecycle faster and faster

While insurers still may feel fairly comfortable with their current core competences and strategy approach, the ever-increasing pace of technological development is a ticking bomb waiting to explode in the insurers’ technology ecosystem

Combining all the factors, adding the New Normal of digital engagement caused by the pandemic, the fact that core competences are rendered useless overnight, the existence of IT in all elements of the value chain and the change of software and application development speed, suggests a change in the approach to creating the insurer’s strategy

The new approach to strategy should be focusing on the current and projected impact of technology even before analyzing the internal and external environment, creating the SWOT and defining core competences

Figure 4: The impact of technology sets the starting point for the strategy discussions

IT on the permanent Board agenda

Understanding the technological development with the current and future impact on the insurance industry and on the insurer specifically is crucial to setting a strategy and even to navigating the operational environment on a daily basis – and the importance of the head of the insurer’s technology (CIO, CTO, CDO, etc.) cannot be emphasized enough

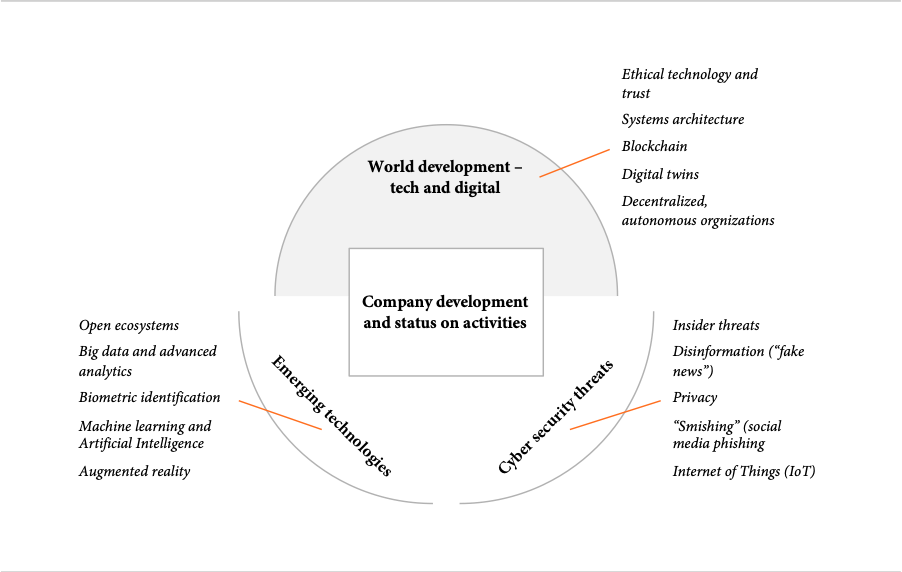

The impact of technology has to be on the permanent agenda of the Board, adding the following agenda items for the technology lead to present:

• What’s going on in the world?

• What’s going on in the company?

• Cyber security, are we at risk?

• What’s the impact of emerging technologies?

A great starting point for the discussion is a brief run-down on latest, relevant tech trends, technology and new ways of designing and distributing products as this will keep the Board up to speed with what’s going on in the world and spark a necessary discussion on whether (more) change to current strategy is required

The head of technology is involved in most processes and developments within the insurer and is therefore well positioned to continue the brief to the Board with a short update on what’s going on in the company from a digital perspective, relating ongoing or planned initiatives to the (digital) developments in the operating environment

Figure 5: Adding Tech to the strategy and Board agenda

An agenda item that require special attention is cyber security, emerging threats and actions already taken or required to be taken. Cyber security threats are increasing at the same speed as the technological development and require constant attention by the entire company

Lastly, a brief update on emerging technologies and their impact on the insurance industry – as well as threats and opportunities for the insurer – could spark a healthy debate on whether the current strategic direction need to be adjusted to accommodate the expected impact

The addition of tech overview and implications to the Board agenda and approach to strategy adds additional responsibility to the head of technology role. Assuming that a part of the job is already keeping up to date with technology trends and development, the addition to the role will most likely be a strategic and analytical perspective and the capability of relating the analysis performed to the current situation of the business

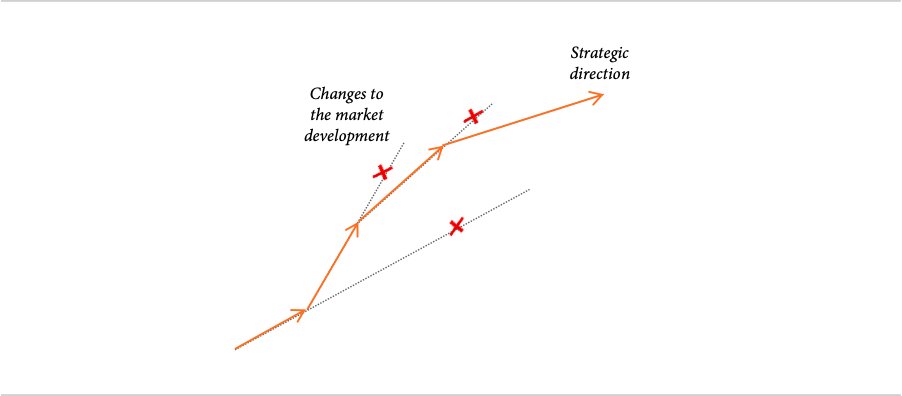

This enables the head of technology to engage in discussions on how the technological development is likely to impact the insurer and suggest ways to leverage opportunities and mitigate risks – and provide the critical point of departure for formulating the insurer’s strategies going forward

Figure 6: Constant monitoring and assessing the implications of the tech development enables the head of technology to suggest changes to the strategic direction of the insurer

In a fast-moving digital world, the winners will be insurers that sense the change and responds accordingly, constantly making changes to the strategic direction of the company to make the direction match the market development

A look into the future

Predicting the exact future of the insurance industry is impossible, but it should not stop us from trying, as it is required to have a “best man’s best guess” indication in order to create a strategy ready to take on the future challenges in the market

Examining the frontrunners in the insurance industry, what’s trending in insurtech and fintech and where the general technology development is headed, will give a quite clear indication of the tech mainstream development over the coming years

Pairing this information with trends in consumer behavior creates a great starting point for crafting a picture of the future for the industry

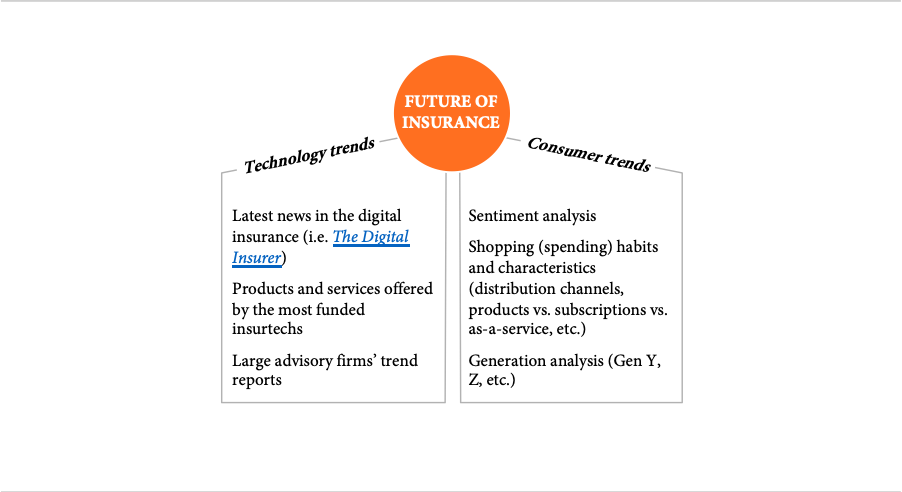

Figure 7: Sources for trend information for technology and consumers

Figure 7 provides an example of where to look for technology and consumer trends that will have an impact on the future of insurance. Some major trends that are clear at the point of writing are:

• Individuality. Consumers expect personal attention and custom-tailored products; they wish to express themselves through their product choices and they expect personal attention from the companies they deal with

• Here-and-now, and not more. The virtualization and digitization of the world caused by the pandemic accelerated an already present need; consumers want their products immediately and do not want to wait – adding to this, they only want exactly what they need and for the specific time they need it – think pay-per-use, as-you-use and subscriptions

• Artificial intelligence (AI) and Internet of Things (IoT) are technology advancements that cater to the above two consumer trends, allowing companies to combine products and services exactly based on consumer demands (AI) and behavior (IoT)

• Blockchain and parametric insurance, specific insurance products build on smart contracts that get executed if a certain event is triggered, challenges the business model of most insurers as these products, for now, are sold as add-ons to other products and services with little or no direct contact with the insurer

• Hyper-connectivity. The world is becoming increasingly more connected and consumers are used to being always on – and they expect all their devices to be synchronized and easily connected to whatever gadget they may have, including pets, refrigerators and hoovers

More trends and developments will impact the insurance industry now and in the future – the above are mentioned as they almost certainly will have a massive impact. In fact, many of them are already driving insurtechs to develop new products and services, so insurers should take note and prepare for this future now

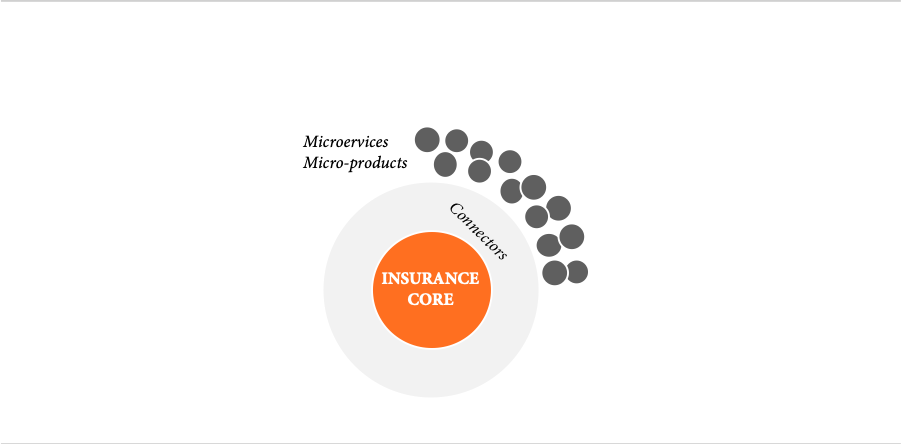

For insurers, even the consumer trends are depending on technology, as it would be virtually impossible to accommodate the needs for individualization and tailor-made products without proper IT systems to build and provide this to the consumers

In a hyper-connected, on-demand environment, insurers are forced to rethink their technology architecture to deliver what the consumers are looking for. Creating this kind of tech architecture is no simple task as both products and ways for partners to connect has to be broken down to atoms

Consumers want on-demand products that are individually tailored to their needs. The insurance products must therefore be broken down into smallest possible bits so the consumer can pick and choose exactly the covers, limits, time period and services needed – not ‘build your own pizza’, but ‘build your own insurance’

Since tailoring your own insurance could be time consuming and require a certain level of insurance knowledge from the consumer, artificial intelligence must work together with the consumer to create the ‘perfect-match’ insurance products

This could also be a great opportunity for partners or platforms, that via access to the micro-products through microservices can create their own, custom and value-added versions of the insurance product and distribute them through their platforms

Catering to the distribution platforms and ecosystems, offering a very easy way of connecting and designing products tailored for the specific customer segment of the platform or ecosystem is becoming vital as significant shares of global sales are gravitating towards these channels – McKinsey suggest 32 % of all global sales will be through ecosystems and platforms by 2025

Few insurers have already taken the first steps in this direction and created API-sandbox environments where partners can access the data required to issue their own policies on the insurer’s behalf – without interacting with the insurer at all!

Figure 8: The technology architecture of the insurer must be flexible enough for customers and partners to create their own products

Offering micro-products through microservices does not only demand a significant redesign of the insurer’s tech architecture – the entire organization must be capable of delivering services in an ultra-flexible way, and at same pace as the development of the environment

Please refer to the whitepaper The unknown next – building a future-proof operating model for the insurer for a walk-through on creating a target operating model capable of coping with an uncertain future

The future of IT is divided

Expanding the scope of the insurer’s IT unit suggests splitting activities and priorities into two, interdependent, areas, IT as business driver and IT as business support

Throughout this whitepaper, the discussion has been focusing on IT as business driver, understanding how the unit can bring competitive advantage to the company by thorough market understanding, followed by impact analysis and recommendations to leverage or mitigate risks and opportunities arising from the market development – and following this, implementing whatever actions are decided

The other important function of IT is to keep applications, systems and infrastructure running, from servers over internet access to telephony – it all lies with the IT department and is as vital a task as driving the business through business innovation

Two-speed IT

Most insurers struggle with legacy IT systems, custom-built decades ago, or standard systems that has been patched and modified significantly over the years. In both cases, the tech architecture of the insurers is complicated and cumbersome to change at the scale needed if the insurers are to stand a chance in the volatility of the New Normal

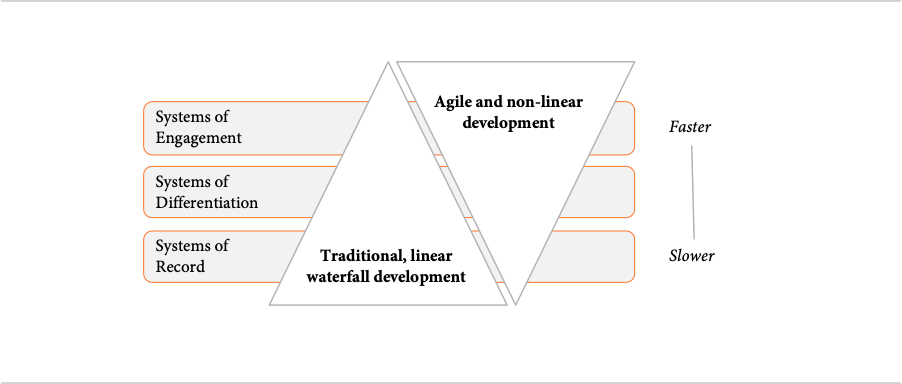

It is rarely feasible – nor advisable – to change all systems and build an entire new core system at once, as this would require too many IT and business resources to make it a viable option. Instead, it is worth looking at Gartner’s model for bi-modal IT that basically suggests dividing the IT systems into two, fast IT and slow IT

Fast IT is – as the name implies – IT and technology that can be developed and deployed fast and in an iterative way, securing optimal connection with the changing needs and demands of the marketplace

On the top of Fast IT are Systems of Engagements, that are the applications and services communicating directly with partners and customers – for example websites, API sandboxes, mobile applications etc. The top layer requires constant and fast changes to follow the market development

Figure 9: Gartner’s bi-modal IT concept for dynamic IT development with legacy systems

Below the Systems of Engagements are Systems of Differentiation which holds most of the insurer’s digital intellectual property – this could be specific underwriting models or the capability of allowing customers and partners to tailor-make their own insurance – this layer will still need to be flexible, but changes are typically larger and require more testing before publishing

An error in the Systems of Engagement layer is not as problematic as an error in the Systems of Differentiation layer can be

Slow IT refers to core applications that cannot – and should not – be changed frequently

Financial transactions and core policy information are the backbone of the insurer and are part of the Systems of Record that is the lower layer in the bi-modal tech architecture model. Changes here are critical and cannot have any chance of error as this would jeopardize the operational foundation of the insurer

Systems of Record are therefore slow to change as all changes have to be meticulously planned and tested to reduce any risk of mistakes

A technology architecture building on the bi-modal principle allows the insurer to go to market relatively fast with innovations and new products and services while preserving the legacy core – this is typically a more cost-effective, and faster, way to modernize the tech architecture

Build vs. buy

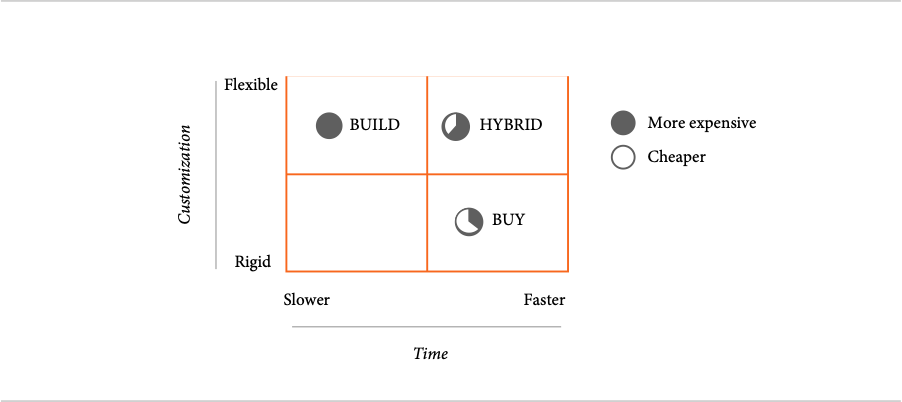

A logical follow-up question to a decision on implementing a bi-model architecture is whether the applications should be built by the inhouse IT teams or bought as an out-of-the-box turnkey solution

Broadly speaking, turnkey solutions tends to be faster to implement and launch, where inhouse development takes longer time to launch – and typically comes at a higher cost, mainly caused by the development time

However, applications built inhouse will be more flexible and meet the exact demands of the insurer, where bought, ready-to-launch systems will not have the same flexibility and may require operational adjustments within the insurer

Figure 10: There are many factors affecting whether to build or buy all or parts of the insurer’s tech architecture

Building the applications inhouse can be an important part of creating new core competences for the insurer, but it is worth noting that the sheer combination of various turnkey solutions can provide a core competence or competitive advantage as well

Depending on the application being developed, a long(er) time to market caused by inhouse development may risk the application being outdated even before it is launched, which is another important consideration when debating whether to build or buy the future IT systems

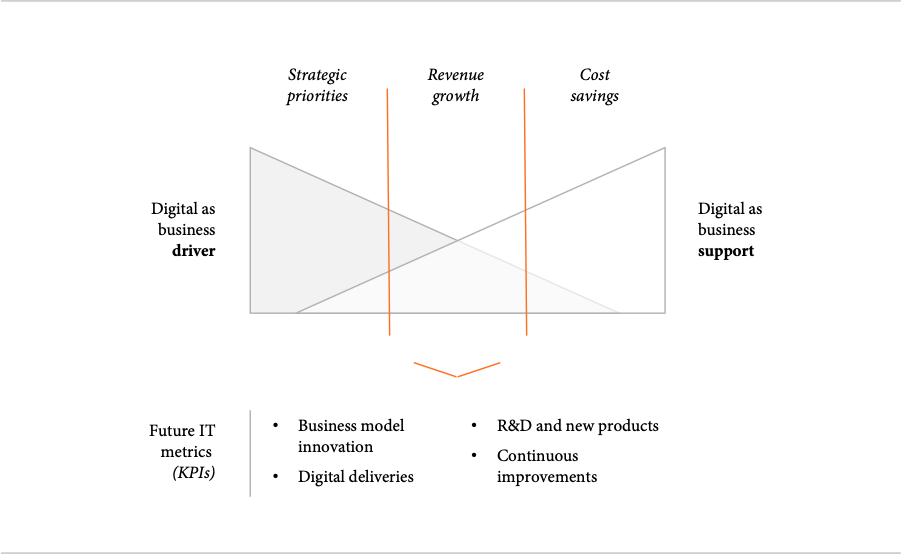

Metrics – how do you measure IT?

A redefined focus of the IT unit requires a set of redefined metrics to measure the overall performance of the IT unit. It is no longer sufficient to look at cost of IT per employee (what happens when automation replaces jobs?) or systems availability

Broadly, the deliverables of the ‘new’ IT unit can be divided into four main areas:

• Business model innovation

• Digital deliveries

• R&D and new products

• Continuous improvements

All four metric areas should be directly related to either the strategic priorities, revenue growth, cost savings or a combination of these

Metrics describing business model innovations could be redesign and digitization of current operational processes, optimizing internal workflows or enabling new distribution channels to sell the products and services. Specific measures can be time saved with new processes or revenue generated from new distribution channels

Figure 11: New metrics to track performance of the IT unit going forward

Digital deliveries are quite straightforward and covers projects completed across the organization where KPIs could be shared with the project owner (sales increase, reduced turnaround times, improved customer satisfaction etc.)

The same goes for R&D and new products, that also are fairly easy to define and measure. R&D is typically measured as a percentage of the overall IT budget and new products can be easily measured as ’new products introduced’ and their contribution to the strategic priorities, revenue or cost savings

Last is the ‘business as usual’ category, the continuous improvements that – as the words says – measures how IT contributes to the daily operations of the insurer. This is where KPIs as systems and application availability resides and may also include KPIs for improving various areas of the IT operations, average project delivery accuracy, server downtime etc.

Final thoughts

This whitepaper essentially suggests that the new core team at Board meetings is the CEO for overall reporting, the CFO for finance and risk compliance reporting and the head of technology (CDO, CIO, CTO…) to provide a status of current market developments, implications and ways to leverage opportunities and mitigate risks – a regular strategy review

Changing the team meeting the Board, let alone the organizational ‘power’ it adds to the head of tech position, is new to most insurers and existing management structure. Furthermore, the corporate culture and complacency will make it difficult for the CEO to change – and the change obviously needs to come from the CEO

A major reason for this reluctance is the CEO is not fully convinced about the pressing need for adding the head of tech to the ‘inner circle’ of power, and this reluctance can prove dangerous for the future survival of the insurance company. It’s that serious. And it must happen now

Every journey, small and large, begins with a first step. I hope reading this whitepaper is yours