Digital transformation; strategy, processes, culture and hard work!

• Digital transformation is a way to keep the insurer competitive

• It is centered around the processes of the insurer’s ecosystem and is all about as-is and to-be processes

• Begin simple and scale based on the successes from the first projects

• A cleaned project portfolio provides a strong starting point for digital transformation

• Be aware of the risks and how to mitigate them

Digital transformation as a concept – or phrase – has been used extensively over the last years, and almost all new projects involving IT and digital has been labeled as digital transformation projects, so the concept has become diluted and the original ideas behind the term unclear

The lack of clear definition – or at least consistent use of the term – lends to increase the confusion about what digital transformation is, which creates a haziness around the concept and makes it unapproachable and mysterious to many insurers. We feel it is something we need to have or do, but are uncertain on how to do it and what it actually means

Instead of providing yet another definition of ‘digital transformation’, describing the purpose of digital transformation projects makes good sense – this will help understand the ‘why’ of digital transformation

In short, digital transformation is what we do to prepare the insurer to cope with the anticipated future market developments and competition. Digital transformation is therefore a tool, or methodology, supporting the insurer in reaching the strategic targets – this is important to remember

Basically, strategy is the process of understanding value and defining how to provide it. This covers value to shareholders, customers and partners, and sets out the path to maximizing the value delivered during the strategy period

The insurance industry has historically been quite resilient to market changes and even the talks of and focus on disruption of the industry by insurtechs has not (yet) materialized into any major changes to the basic industry construct

However, the outlook for the future of the insurance industry indicates that things may be about to change and that the winds of change will be blowing over the industry sooner than anticipated – Figure 1 provides an overview of the factors that are expected to accelerate the changes within the industry

Figure 1: Overview of the factors that are projected to influence the acceleration of the insurance industry development

Placing the question marks in the right places for the insurer gives an overview of the risk of increased competition or disruption the insurer is facing – and for most insurers, the risk is high, i.e. the question marks will be to the left in Figure 1

Adding to the risk of disruption are the impacts on the world economy from the COVID-19 where the aftershocks have not even been seen yet. In other words, the insurance industry – as well as many other industries – is facing a period with significant uncertainty and market volatility

Figure 2 below provides a summary of most likely (if not already confirmed) impacts of the COVID-19 and existing trends that are growing faster because of the pandemic

Figure 2: Impacts and trends forming the insurance industry now and in the new future (source: The insurer of the future needs a new base construct and sustainable core competences)

It is time to act, and digital transformation is at the heart of enabling the insurer to cope with the next level of industry competition and unknown future market fluctuations

The digital transformation framework

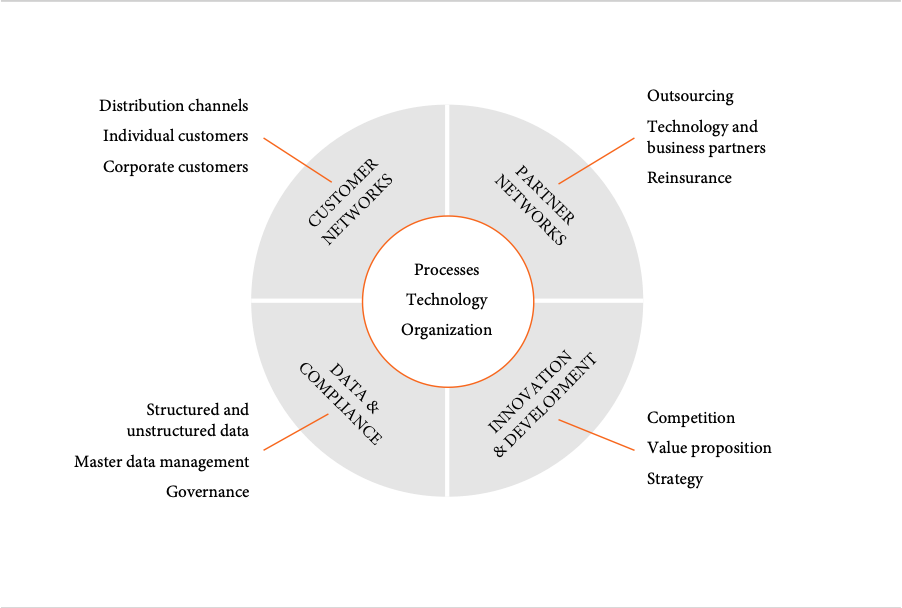

Understanding digital transformation requires looking at the insurer’s ecosystem; the internal and external network and processes that ultimately defines the insurer and enables the company to run the business

This is important because digital transformation touches all elements in the ecosystem, and the digital transformation projects should be defined and prioritized on a basis of where change is most needed – it rarely makes good sense to transform all elements in the insurer’s ecosystem at once, as we’ll discuss later in this whitepaper, so a phased model based on prioritization is needed

Digital transformation is in essence a change and optimization of all external and internal processes in the company, aiming at making them smoother, faster, with fewer touchpoints and, of course, digital. The emphasis is on transforming the processes and to be successful, the focus must be on the transformation part much more than on the digital and technology parts

In the center of the insurer’s ecosystem is the core, the current processes that defines the company’s operating model, the technology supporting the processes and the organizational structure, and people enabling the insurer to operate. Processes can be well-documented and formalized ways of doing things, and they can be informal, implicit elements of the company heritage and culture

Technology is everything digital that runs in the insurance company, including the office software packages that enables employees to write mails, documents and presentations. It also covers the technology and information architecture, for example the core database systems, internet connectivity and quick-and-dirty solutions (hacks) made over time to support the business

The heart of the company is the organizational model with formal and informal hierarchical structures, silos, bureaucracy, company culture, incentive programs, and, people. This is the most complex part of any company to fully understand let alone map out and define as part of the transformation work

There are so many unwritten and informal rules, traditions formed by history and time, as well as hidden power networks of employees playing a vital role in the daily operations of the insurer, that it can be very difficult to understand the real processes of getting things done

Understanding the processes, formal and informal, of the insurer is key to working with any kind of company transformation and therefore plays a very important role in working with digital transformation projects – failure to understand how the company works makes it very difficult, if not impossible, to implement any new or revised processes

Figure 3: The insurer’s ecosystem of partners and processes

The customer networks cover the processes of acquiring, servicing and renewing direct, indirect, corporate and individual customers. It also covers the distribution networks and the way the insurer interacts with brokers, agents, digital platforms and all other ways for the insurer to reach the customers directly or indirectly

Virtual interaction with customers is in full focus following the pandemic, and insurers are rapidly building digital interfaces with customers to enable a full-fledged digital service offering. This has increased the focus on the insurers’ websites and other digital communication channels, but many of the efforts are falling short of the expectations

One of the major reasons that digital customer interaction projects fails – or doesn’t deliver what is expected – is the insurer’s processes. The team will be working on ‘what can be seen’ by the customer (and management) and concentrate their energy on the front-end website and processes in direct contact with the customers, and not pay sufficient attention to all the secondary and tertiary processes that are required ‘behind the scenes’ to provide a smooth front-end customer experience

Ensuring all relevant processes – front, end and in between – are revisited, adjusted and digitized is therefore key to making digital transformation projects a true success. Only a complete revamp of all processes involved will deliver the expected outcome of a faster, smoother and easier digital customer experience

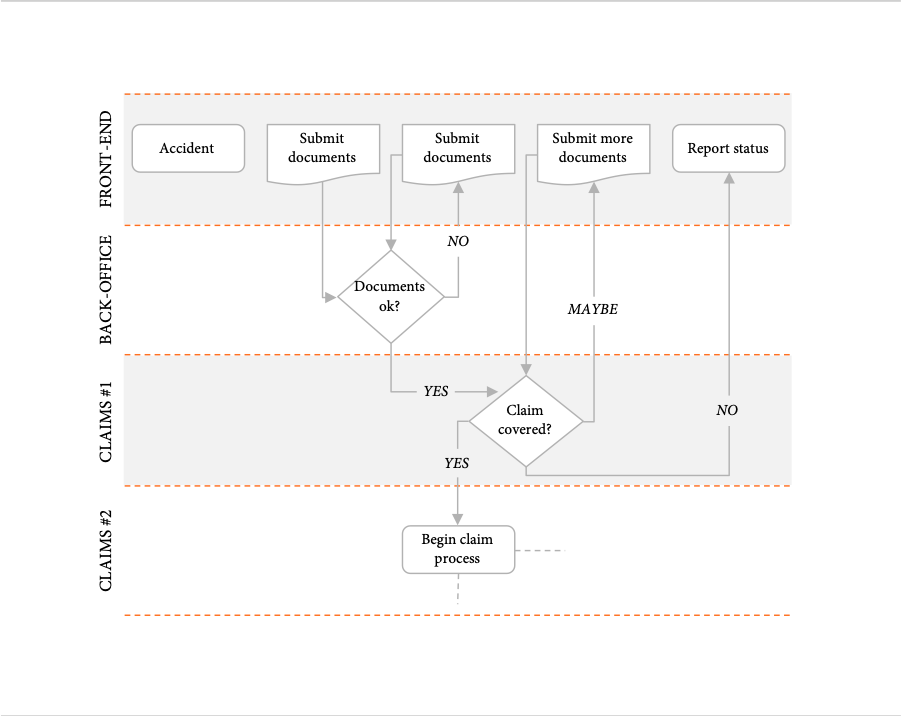

A simple, but effective, tool to map out all processes and secure no processes are left out, is the swim lane diagram that can be used to understand what processes, business units and teams are actually involved in handling the overall process (i.e. filing a claim) – an illustrative example of the swim lane diagram is shown in Figure 4

Figure 4: The swim lane diagram is used to map all sub-processes and units involved in delivering one service to a customer, for example submitting a claim

Each ‘swim lane’ in the diagram represents a business unit, a department or a team within the insurer, and the boxes and arrows indicate relationships between them, and decisions required for the process to continue

When mapping processes as they are, it is not uncommon to end up with very complex swim lane diagrams – and this is exactly where the value of the digital transformation can be found; reducing these complex diagrams to processes as simple and digital as possible

Using swim lane diagrams is not only for mapping the processes around the customer networks, but the customer interaction is the area where most efforts fail because the focus in many cases is restricted to the front-facing processes and not on all the underlying processes supporting the customer interaction

Similar methodology should be used when understanding the processes and dependencies between the insurer and its partner networks. The insurer’s partner networks are the external networks that are part of the insurer’s overall value proposition and as such covers a wide range of partner types, ranging from reinsurance companies over technology providers to outsourcing partners for non-core activities

Please refer to the whitepaper The unknown next – building a futureproof operating model for the insurer for a discussion on how to determine what activities can be outsourced to create a more resilient and flexible insurance company

Connecting seamlessly with key partners plays an important role in the establishing a strong value proposition for the insurer and creating a long-term sustainable competitive advantage in the market. Automated processes between the insurer and partners help reduce response times and improve the overall customer experience, which are both factors that left unattended can reduce the insurer’s competitiveness and open for new market entrants –please revisit Figure 1

The rise of insurtechs in the industry opens up for new and interesting partnerships between the insurers and innovative tech companies, many of whom are building a business model in the insurance industry based on the deconstruction of traditional insurance products (usage-based insurance products, deconstructed into time units and variable covers with variable limits during the policy period)

However, as discussed in the whitepaper, Insurtechs, a part of insurers’ digital transformation?, it does take planning and adjustments to begin working with external partners for the insurer’s product development and – again – digital transformation is key to enabling partnerships like these, reimagining the insurer’s processes to align with the partners, but also to enable the internal operations of the insurer to handle the new ways of working

Many insurers have separate product development processes for each line of business – and some even on individual product level within the line of business – even though 80 % of the processes are nearly identical – or could be made identical. The ‘could be’ is crucial here; many processes are at the onset determined by the teams to be unique and hence cannot be easily transformed, but this is rarely the case in practice

The processes are labeled unique because of complacency and the existing teams’ inability (or unwillingness?) to look at the existing processes in a new light. Experience shows that, in most cases, even major process changes require minor changes to the organization and that it is more often the organization’s resistance to change that hinders the redesign and digitization of the processes

Redesigning the processes around product innovation and design should be based on a thorough market understanding and a clear strategy on where to play for the insurer. The definition of the insurer’s targeted market positioning will be a heavy influence on how the innovation and product development processes should be designed

There’s a big difference in underlying process design between an insurer with a strategy of being a fast and nimble player in the personal lines market and an insurer focusing on big-ticket insurance business from large corporations

Beneath and around customer and partner networks, the way the insurer manages product development and innovation and internal processes and tech architecture, are data and data management systems. Insurers have access to much more data than they currently are capable of leveraging, and this is a huge business opportunity and a risk at the same time

Not knowing what data are available is a risk – how can the insurer guarantee sufficient data security and customer information protection if data available and location is unknown? On the other hand, used correctly, the incredible amount of data available can be used to improve the business in several areas, from better risk understanding and underwriting to substantial improvements in customer service

Regardless, the insurer must be capable of mapping the data before considering – or being able to – leveraging the information, and this should be one of the starting points of any digital transformation project as all processes being redesigned and digitized will rely on data

Building new processes without a full understanding of available data and their architecture risks the new processes being ineffective and in some cases in need of another redesign when the data structures change. Mapping and cleaning data are therefore great starting points for a digital transformation journey and, if done right, can free resources that can be added to the digital transformation projects

Redesigning the processes

Digital transformation is in the most basic form a redesign of key processes in the company with the target of making them digital and significantly simpler, and with less ‘roadblocks’ in terms of approvals, manual intervention and unnecessary bureaucracy

As discussed in the previous section, the typical approach is to carefully map the existing processes as they are in full detail, and with all involved business units, teams and departments clearly described with current roles and responsibilities in that specific process. This is traditionally called the ‘as-is process’

When designing the new and digitally optimized process, the ‘to-be process’, it is important to design the process around the customers and their interaction (journeys) with the insurer. Customers can be internal and external as well as partners and other external business relations

The (radical) new here is that designing processes around customers is in almost all cases cross-functional, meaning that the redesigned process will involve more than one business unit or department. This is radical because it requires an organizational change to succeed, as the newly appointed process owner will need authority to adjust processes and ways of working in the individual business unit or department involved in the customer-oriented process

Figure 5: Successfully implementing new ‘to-be’ processes relies on a new organizational model

Redesigning the processes with a cross-unit ownership allows the insurer to focus on delivering the best possible solution to the customers’ problem or job to be done. Handovers between units and departments are eliminated and information exchange is not required – all relevant information is already in the process, so there is no need to ask for it from the business units before moving on

The process owner will have the authority to change ways of working and processes within each unit to suit the overall process and focus on the customer journey. This is key to making the process future-proof and capable of changing fast to follow changes in customer requirements and market developments

Besides focusing on the customers’ job to be done as a starting point for the process redesign, it is important to ask ‘is this necessary’ questions to each of the stops (approvals, etc.) in the process. Doing this will reduce the number of manual interactions and other elements that slows down the process or makes it unnecessary cumbersome for the customer

Implementing a workflow management system to control the new processes can be a very good idea – this will secure proper adherence to the processes in the organization and provide analytics on usage so potential roadblocks can be identified and dealt with

Where to start – choosing the angle of approach

A key to a successful digital transformation program is to define it as a series of projects to be implemented over time and try to avoid entering into a company-wide transformation program focusing on all projects to run in parallel at the same time

In extreme cases, it may be relevant or necessary to do the all-encompassing company transformation, but it is not advisable as there is a significant risk that there will be too many moving parts to control at any given point. Company-wide transformations require the motivation and engagement from all employees, and the existing corporate culture can make this very difficult to achieve

Planning a digital transformation as serial projects has a greater chance of succeeding for many reasons:

• Easier to plan and manage – sequential projects mean less strain on project resources, and the reduced resource workload delivered by the digital transformation project can free resources to work on the future projects in the pipeline

• Investments based on phases and successful completions – return on investment can be demonstrated project by project which makes it easier to create criteria for releasing investments and resources for the next projects

• Proven success – the organization will see the success of the first project and see the value of the transformation projects, which increases the chances of organizational buy-in for future projects. This require frequent communication from the digital transformation group to have the maximum effect

The above considerations should be considered when planning the starting point for the digital transformation. The most common first project is transforming and digitizing one specific process or the processes within a business unit or department of the insurer. This approach makes the project manageable for a smaller team and increases the chances for a fast success to continue building the digital transformation of the insurer

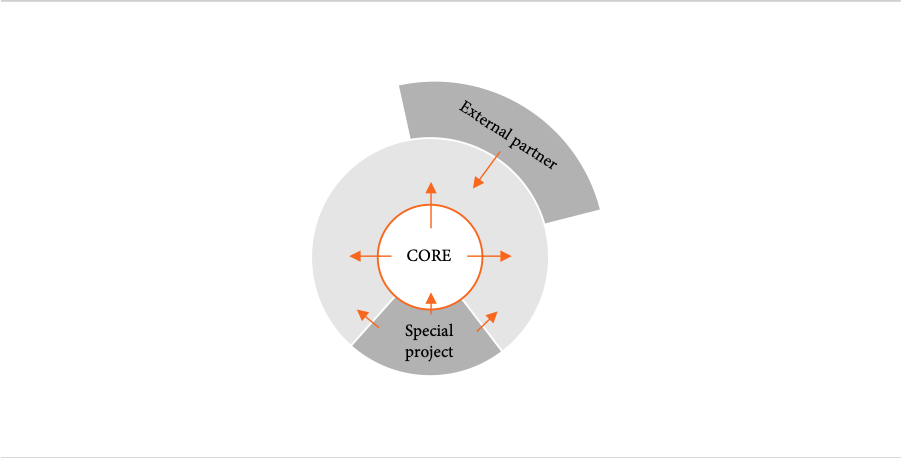

Figure 6: There are several different ways of beginning a digital transformation project

Transforming the core of the insurer does not have to be as profound as it may sound at first. As is the case with the process or business unit, the digital transformation of the core can be focusing on one or more processes, for example how to gather, validate and store customer data or how to ensure correct and consistent new product development within the core systems

Working on the core of the insurer will – since it is the very core of the business – have higher stakes and will most likely require a larger team to run the project as this will have an impact on all units in the company. Because of this, the upside of a successful project will be greater, as most of the company would have been involved some time during the project

Another interesting angle to starting the insurer’s digital transformation is to find an external partner with complementary products and services that, if integrated with the insurance company, would provide a competitive advantage. In this case, the digital transformation project would be focusing on redesigning and aligning the processes between the partner and the insurer

The whitepaper Insurtechs, a part of insurers’ digital transformation? discusses how to effectively work with external partners and how to identify the right processes or elements in the value chain to work with for the digital transformation project

Approaching the digital transformation with external partners may be more difficult than the other angles as the organization would be expected to resist the process changes because they’re not from within the company itself, and therefore are more likely to be seen as a threat by the employees

How to start – cleaning the project portfolio

Regardless of the chosen point of departure for the digital transformation, it will be a project, or projects, of significant scale so the organization must be ready and prepared for this, so sufficient resources can be allocated to the digital transformation project and make it successful

It is therefore advisable to – even before the digital transformation project group has been formed – perform a proper and thorough cleanup of the existing project portfolio. Most companies have built up a quite significant project backlog over time, and cleaning this up by prioritizing and canceling projects companywide provides a great overview of the organization’s capability to take on new projects

If there are too many projects taking up the resources, segmenting the projects into their impact on the business and the estimated project size is a good way to get an overview and selecting which projects can be cancelled or put on hold, so resources can be freed for the digital transformation project

Projects can impact the business in one of four ways

• Increase the revenue (cross-sales, new business, underwriting, etc.)

• Reduce costs (operating expenses, claims, etc.)

• Support a strategic target (increase employee happiness, improve environmental footprint, etc.)

• Secure the insurer complies with regulations

The project size is measured by a combination of the resources it takes to complete and the expected time to complete the project – these two factors are typically closely related

The projects’ placement in the matrix in Figure 7 gives a good overview of the type of project and suggests which projects can be cancelled. Projects with high impact that are small in size could be prioritized to finish off quickly and provide a quick-win for the insurer, where projects with low impact and large in size should be considered cancelled

Figure 7: Classifying projects after impact and size helps prioritization and to find ways of freeing resources

Small projects with low impact could be considered put on hold to make room for the digital transformation projects and high-impact, large projects would typically be the digital transformation projects as they would be transforming the business

Regulatory projects have to be done regardless of size and impact

Remember to note down project interdependencies, as you may find projects that are suggested to be cancelled or put on hold are necessary to complete in order for higher priority projects to be done. These interdependent projects can be added together into one project in the overview to provide a more accurate segmentation of the project

Risks and mitigations

While it is beyond the scope of this whitepaper to discuss project management risks and mitigations for large-scale business and digital transformation projects, it is important to highlight the organizational risks that any digital transformation project faces. These risks can be even more disruptive than the complexity of the project itself and it is necessary to understand what they are and how they can be mitigated

If there is no sense of urgency for the digital transformation project to be completed, it is very difficult recruiting the right employees to work on the project – they will most probably not be released from their existing roles, as their managers don’t see the importance of the project and the employees themselves will not be motivated to work on a project that does not have full support

Figure 8: Most important organizational risks that digital transformation projects are facing and their mitigations

Not feeling the urgency to complete the digital transformation can come from sheer lack of knowledge in the organization. If the top management does not have the sufficient understanding of how the business environment is developing and that significant changes are required to keep the insurer competitive, it is difficult to create an understanding of the need to change, which also results in difficulties finding the people and support for the digital transformation project

The results of a digital transformation are in many cases new and digital processes that run across business units and departments with a process owner in charge of the process as well as the sub-processes in each unit and department. In effect, the unit or department management will lose the full control of their business and this will cause resistance to change from many managers – and risk slowing down the digital transformation project significantly

Successfully managing a digital transformation, large and small, require talented employees that know about process design and optimization, project management and organizational culture. Not many insurers are having many employees with the needed skills, so lack of talent to run the digital transformation projects can also be a risk reducing the impact of the projects

Getting it right from the get-go

Being aware of the organizational risks attached to a digital transformation project is a great starting point as it is possible to mitigate the risks and reduce the probability of the project failing and missing the targets. Digital transformation is a top-down project, so top management must commit completely to the transformation to make it a success

A great way of publicly demonstrating the commitment is to set a ‘North Star’, a guiding principle, for the digital transformation project and maybe even for the future direction of the insurer too. The North Star can be used in internal and external communications and provide the employees working with the transformation project and sense of purpose as they will see and understand the target state of the insurer, and how the projects will help reaching the target

Another important preparation for the digital transformation of the insurer is to make sure all stakeholders have sufficient knowledge about the current industry situation and understand the need for change – sometimes it makes good sense to hire an outside expert to give an industry overview to increase top managements’ attention and knowledge

The starting point and ambition of the digital transformation project has already been discussed but it’s worth underlining the benefits of starting in a smaller scale, as this will allow the organization and its commitment to grow alongside the development of the projects and hence create the support needed for successful project implementation

If the insurance company does not have the right skills to run a digital transformation project, the insurer can find ways of increasing the skills and competences within the existing workforce or employ outside talent with proven experience. Engaging with consultants to run the project can be a solution too, but it is advisable to have inhouse experts to secure consistency in future projects and keep the learning within the organization

Hiring outside experts to work on the digital transformation faces the same risk as working with external partners discussed before; the organization may resist as it is a person coming from ‘the outside’ to start changing processes and ways of working. To be successful, new hires need the full support from top management and the transformation team

Constructing key performance indicators for the successful implementation of the digital transformation projects is a strong way to align people throughout the organization. If the targets are defined clearly and tied to financial incentives, employees will be focused on working towards the targets and this will help the cross-unit collaboration

Final thoughts

It is more important than ever for insurers to change their operating models, so they’re better equipped to navigate in an unknown and volatile future. Digital transformation has long been touted as the only right thing to do and that insurers should do a complete transformation of the company

While it is correct that most processes and ways of working would benefit from an analysis and redesign, it is important to begin the transformation at a scale where the organization will be capable of ‘keeping up’. Experience has shown that too many projects launched in parallel will make them all fail because the organization do not have the sufficient manpower to give the required attention to each project

A far better approach is identifying the processes and ways of working, that will return the greatest benefit by being redesigned and begin here. Based on the success of this project, other projects can be rolled out gradually and as the organization gains the knowledge and experience, an increasing number of projects can run in parallel

The most important is to get started. Every journey starts with a single step. I hope reading this whitepaper is yours

Good luck